Doing Mergers & Acquisitions (M&A)

Safely in a Declining Market

How to Catch a Falling Knife - Safely Buying Companies in an Economic Downturn

Table of Contents

The current COVID-induced recession, whether short- or longer-term in nature is and will continue to create potentially interesting opportunities for Buyers and perhaps more difficult times should you be a Seller.

In this newsletter, we’ll offer our perspective on how to explore potential buy-side opportunities and, if you’re a motivated Seller, what you’ll likely be asked to consider by prospective Buyers along with how to proceed if you are a Seller.

The M&A Landscape, Pre-Pandemic

Up until early March of this year, M&A in the IT Solution Provider eco-system was riding a near decade-long upsurge. Offers were nearly all cash, with small escrows to cover Representations and Warranties or, increasingly Buyers and Sellers were splitting the cost of Rep & Warranty Insurance and the transactions were truly all cash.

Deals were closing quickly, often in under two months, since Buyers were increasingly efficient in getting through due diligence.

Little if any of the due diligence contemplated a pandemic and what would happen to the acquired company (and indeed the Buyer) under a pandemic-inspired recession.

The Mid-Pandemic M&A Landscape

The pandemic has had an immediate and profound impact on M&A. Many, perhaps most of the M&A transactions under Letter Of Intent (LOI) have been put on hold, as Buyers are increasingly unable to effectively value companies they had under LOI; and since many Buyers are now having to husband the very cash they need to close on acquisitions. We’re increasingly seeing Buyers, both Strategic (i.e., Solution Providers) and Financial (e.g., Private Equity Groups, “PEG”) asking Sellers to put a substantial portion of their total consideration into an earn out to more effectively protect the Buyer; this may even take place where an LOI has already been executed. Those deals being completed or continuing on track appear to be either for platform investments – a scarce commodity even in a pandemic – or tuck in acquisitions that remain attractively priced even under a recession outlook.

But some astute Buyers understand the old adage “buy low, sell high” and retain sufficient financial strength to not only continue to acquire under the current conditions but to do so aggressively. Indeed, one PEG told us that their 2007 fund, which was largely invested during in the 2008 – 2009 recession, was their all-time best performing fund and they intend to emulate that performance by investing aggressively across all their funds in the current recession. A leading large Solution Provider and serial acquirer also told us recently they were going to be actively, and aggressively, seeking bargains.

Indeed, we’re hearing from many clients that they’re receiving a sudden increase in the number of inbound calls from prospective Buyers. This is not surprising as many Buyers have been unable to get Solution Providers to respond and likely now feel their calls have a higher probability of being returned.

And we believe these Buyers are right, there will be bargains and if prudently priced with terms and conditions that protect the Buyer, more so than the Seller, this is unfortunately a unique buying opportunity.

The Service Leadership Index® Financial Early Warning Score™

At Service Leadership, we benchmark a large population of Solution Providers and as such have a unique window into the health of the industry. We have built a metric we call the Financial Early Warning Score™, or FEWS™. It is comprised of weighted evaluations of the Solution Provider’s:

- Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA),

- Current Ratio (a common Balance Sheet ratio) and,

- The proportion of their operating costs covered by the invoices they issue for their monthly recurring Revenue contracts.

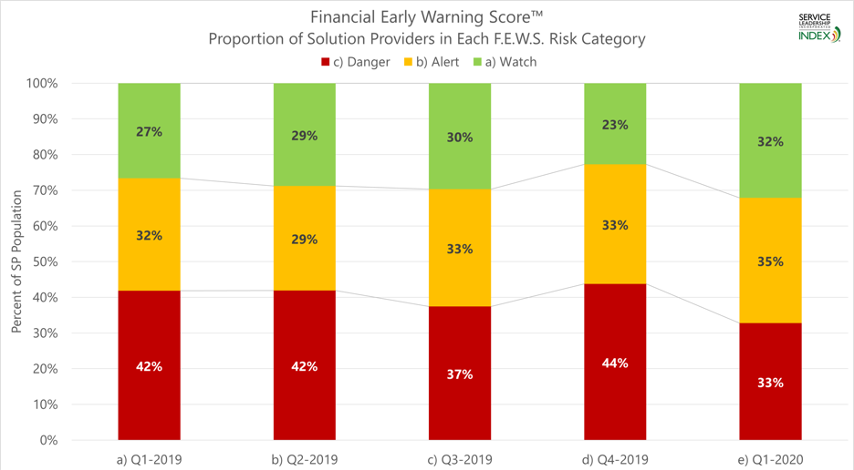

Coming into the pandemic which hit in earnest in Q1, here is the distribution of the FEWS scores across the Solution Provider industry:

Figure 1 - Distribution of Financial Early Warning Scores in the Solution Provider Industry

The year 2019 was a strong year for Solution Providers in general, building on 2017 and 2018 which themselves were strong. How then, could the fourth quarter of 2019 have the most Solution Providers in the “Danger” category and fewest in the safest category (“Watch”)?

The answer is mundane: To reduce their tax burden, Solution Provider owners, as with many business owners, take steps to reduce profitability and cash on hand in the last quarter of the year. Two of the three components of the FEWS score are impacted by these. Hence, more appeared in the Danger category.

The COVID pandemic began to materially impact the global economy in the first quarter of 2020. How can the FEWS scores in Q1-20 be the best of the five-quarter period? The answer won’t surprise many Solution Provider owners: Q1 was a good quarter for many Solution Providers. To the extent that expected Revenue was impacted by clients reining in IT spending, it was often offset by unexpected Revenue from helping clients urgently adopt the Work from Home coping tactic.

Yet, despite the strength of 2019 and of the first quarter of 2020, still a third of Solution Providers have little in the way of a safety buffer to manage into and through a recession.

As such, those not generating positive net income from March onwards need to make changes to get to positive cash flow as fast as possible (within weeks); they simply do not have time to sell their way to profitability. They’ll also need to enact payroll and other cuts soon (within weeks). These cuts likely include reductions in both Selling, General & Administrative expenses, as well as Services COGS (labor).

Some number of those in danger will do too little, too late, or will experience even further reductions in Revenue, will find themselves with the options of liquidation or selling their company. And some number of the Solution Providers who are not in the danger zone, they may conclude that the current recession will require years to recover from and as such they’re better off seeking to sell to a better positioned, stronger Solution Provider to improve their prospects.

We are already seeing motivated Sellers. So, the questions are: Do you want to be a Buyer, and if so, how best to proceed? And should you consider selling and again, if so, how best to proceed? Let’s take each of these questions in turn.

Insights for Buyers (and for Sellers)

Am I Ready to Do M&A, Really?

Irrespective of your desire to embark on one or more acquisition, the prudent Solution Provider (or PEG investor’s portfolio Solution Provider) should always ask, am I ready to do M&A? Really? A few criteria to keep in mind:

- What is your “FEWS” score? Meaning, “Do you have a healthy cash flow, even under a pessimistic scenario?” and “Do you have sufficient financial reserves to invest in M&A now, and still remain safe in your core business?”

- Do you have the expertise and management cycles to not just pursue acquisitions but to successfully and efficiently integrate acquisitions into your business with unduly defocusing your management team and disrupting your current business?

Let’s assume you still want to move forward, what then are reasonable planning assumptions for the businesses you’re considering acquiring? Specifically;

- A “V” shaped recovery (next 3-6 months);

- A “U” shaped recovery (6-12 quarters); or

- A national or global financial “apocalypse.”

In our view you should consider a “U” shaped recovery as your base plan for Revenue planning any acquired company: A “V” is a dangerously optimistic planning assumption and a catastrophe is, well, unplannable. Under a “U” shaped recovery you should consider planning assumptions that include up to a 45% decline in Product Resale, with a parallel upwards of 45%; decline in Project Revenue, and as much as a 20% decline in Managed Services Revenue in the first 2-3 quarters; as some of their customers go out of business, many reduce staff so have fewer users hence lower MRR, and many will ask for a discount or other ways to pay less.

Deciding If the Target is a Falling Knife, and If So, Why is it Falling?

But even with such a significantly lower Revenue outlook for a potential acquisition, how can you be assured that your Revenue plan for them is sufficient and you’re not trying to catch a falling knife?

In our view, it’s critical to distinguish between a high(er) Operational Maturity Level™ (OML™) business which got into a cash crunch and need to sell Vs. a low(er) OML business which is persistently underperforming financially. Start with an interrogation of their financial performance over the past few years, if they were performing well in terms of Revenue growth, Gross Margin performance and bottom line performance but entered the year with unusually low cash reserve and got into a cash crunch, here’s what we’d expect them to tell you:

- Here’s why we have an operationally strong business (i.e., higher OML); and

- We decided to aggressively invest in (e.g., Operations, new Lines of Business, a new geography, and/or in Sales & Marketing); and/or

- Tax planning and/or owner related dividend requirements took most/all of our cash reserves.

But this begs the question of when these owners/executives saw the COVID recession coming, why couldn’t / didn’t these otherwise able owners/executives cut deep enough and fast enough? What you’re looking for are owner/executives who can build a great business but now find themselves unable to lead decisively in a crisis – whether they’re able to discern this about themselves or not. Alternatively, you may have an owner that has simply decided they can no longer afford to go it alone and that there’s strength in size and financial resources.

In contrast, the underperforming owners/executives will have a track record of underperformance across their profit and loss (P&L), typically with anemic top line growth, below average Gross Margins and poor cash flow. These owners/executives may be unable to provide clear or compelling reasons for their underperformance or why they now find themselves unprofitable, out of cash, and unable to identify, much less execute, the steps necessary to survive the current conditions.

These underperforming Solution Providers are typically difficult to successfully integrate in the best of times. As a result, if you have one as a prospect, we would encourage you to consider it not as an “acquisition” but a potential “group hire” of a small distressed competitor going out of business. To manage your own risk, we’d recommend you only consider distressed, low OML prospects that are less than 20% of your size, not bigger. Then buy their customer and prospects lists in exchange for a job for the former owner(s), a small bit of cash and a commission on the purchased accounts for say a year. And even then, get a pre-agreement that you can terminate your choice of customers since these underperforming Solution Providers often have a higher proportion of unattractive customers.

We recognize that some acquirers actually target the low OML underperformers with the thesis that these businesses represent the best bargain insofar as the price is the lowest and these acquirers believe they have the operational and executional prowess to simultaneously acquire, integrate and upgrade these businesses. That’s a very high OML set of skills and not for the faint of heart.

Understanding Your Search Criteria to Minimize Risk

With this in mind, how should you target prospective acquisition candidates, in this declining and recessionary period? First of all, you should seek to minimize the risks and investments associated with integrating an acquired Solution Provider. This means targeting Solution Providers who have comparable:

- Target Customer Profiles (TCPs) (i.e., number of users, buying style, verticals if appropriate, etc.);

- Solution sets, especially in Managed Services;

- Pricing regimes;

- Operational infrastructure and approaches – e.g., same tools (PSA, RMM, quoting etc.).

A matrix serves well to explain these tests:

| Synergy Checklist |

Acquisitions That Don’t Often Work Out Well |

Acquisitions That Most Often Work Out Well |

| TCP (i.e., narrow target customer size range) |

Different TCP (or Buyer and/or Seller don’t have a properly narrow TCP). |

TCP is the same. |

| Tool Stack |

Different |

Same |

| Technology (Client HW/SW) Stack |

Different |

Same |

| Pricing |

Seller’s pricing lower than Buyer’s. |

Seller’s pricing higher than Buyer’s. |

| Geography |

Acquired location(s) farther than the “Distance Rule” (more later). |

Acquired location(s) within the “Distance Rule”. |

| Return on Investment (ROI) Timeframe |

ROI model assumes little room for error in either timeframe or resources needed. |

ROI acceptable even it takes 2x as long and 2x as much resource as originally planned. |

Look for other potentially additive attributes; for example, does the Solution Provider serve verticals that should perform well in a COVID-led recession (i.e., can thrive in Work from Home and/or serve a critical area of the economy such as health care and education)?

There are some commonly-sought synergies which, properly done, can deliver on their goals. However, most often, the Buyer is unaware of the tricks to make sure they happen and to avoid unintended outcomes. Briefly, they are:

| Intended Synergy Goal |

Why This Most Often Doesn’t Come to Pass |

| Add a new TCP |

IT Services do not transport well up and down the customer size range, especially Managed Services. |

| Add a new geography |

Risky; risk partially mitigated by following the “Distance Rule” |

| Add good customers |

If Seller is higher OML, more customers will be win/win; if lower OML, fewer customers will be win/win. |

| Add good people (individual contributors) |

Possible: Depending on OML, between 30% and 90% of people will be valuable additions. |

| Add good managers |

Possible: Same as above.

However: Owners of small Solution Providers (especially MSPs) tend to be technologists, less so business people. If you are a copier dealer, and you are buying a small MSP (i.e. under, say, $4mm in Revenue), likely the owner will not be the right person to lead your IT business unit. |

The Buyer/Seller “Whiteboard Day”

A good way to test your synergy theories, and vet out a number of culture and business operations factors, is the “Whiteboard Day” between the buying and selling CEOs.

The goal of this day-long session is to test the possible synergy, and the Buyer’s and Seller’s styles of conducting business, after Non-Disclosure Agreement (NDA) is signed and before an LOI is offered.

- In advance of the Whiteboard Day:

- Identify five of the Seller’s typical customers (not biggest or smallest), but remove names.

- Identify five of the Buyers typical customers (not biggest or smallest), but remove names.

- Service pricing and offering walkthrough, live on the whiteboard:

- Price the Seller’s five clients with the Buyer’s standard pricing model for the same services.

- Price the Buyer’s five clients with the Seller’s standard pricing model for the same services.

- If offers (packages, features) are 90% the same, that’s good.

- If Seller’s pricing turns out to be higher, that’s good. If both parties’ pricing is the same, but it’s set at low OML pricing, that’s bad. If Buyer’s pricing is more than 5% higher than Seller’s, that’s bad, for two reasons:

- Most of the Seller’s customers will not convert to Buyer’s pricing, saddling the Buyer with the same suboptimal profit model.

- Buyer’s sales people will conclude that Seller’s (lower) pricing is good enough (“Why else would we buy them?”) and attempt to sell future deals at that lower pricing.

- For the same 10 anonymous accounts, identified above, run through: How did we attract them, how did we get a proposal to them, how did we pitch it, why did we win, how did we on-board them, how do we account manage them?

- For the last three accounts (not the same as the five above) that the Seller lost due to their own mistakes, what were the mistakes, how did they happen, and what steps were taken to try to rescue the account?

This exercise will teach both parties much about pricing and packaging, but also about sales model and approach, account management, Service delivery, and business culture in terms of what vocabulary is used and how customers are viewed and treated.

The goal is ease of integration at the lowest cost in the shortest period of time. That said, you also need to be realistic about just how significant the risk of integration is due to defocusing management in a critical time and the required level of investment in time, cash and other resources? It’s important to keep in mind that successful integration represents a substantial effort across most major functional areas of your business and must be done with excellence – which is harder in these times when your business is likely under stress as well.

What follows are guidelines for Buyer CEOs seeking to do successful integrations:

- Tough love is best; slow integrations most often do not work well.

- Pre-acquisition: set measurable goals for 3, 6, 9 and 12 months, and 2 and 3 years. Measure progress vs. those goals and adjust accordingly.

- Acquiring CEO must be a visible and continual leader, especially post-acquisition:

- Over-communicate. In absence of communication, people will tend to assume the worst, so communicate, communicate, communicate.

- Remember, people – even if they love and trust you – can only change so fast. Circumstances may require you to move quickly, but just as quickly as possible you should re-establish a sense of the familiar and stable.

- Make sure the messages your people (and your customers, prospects and business partners) take home to their families are sober but positive and practical.

- Get out in front of customers, prospects and business partners.

- As the acquiring CEO, what to say and not say:

- Don’t say: “Welcome new people, we’re excited to have you. We’re going to pick the best, best practices from each company and combine them into an even stronger company. 1 + 1 = 3!”

- Do say, “Welcome new people, we’re excited to have you. I’m confident that once you learn how we do things, you’ll be great contributors, as I know you have been in getting here!”

- The first phrase unintentionally sets up a competition to prove who has the best, best practices. The acquiring CEO will end up being a tie-breaker on many issues, which is not a win/win position for a leader to be in.

Geographic Considerations

You’ll also need to consider just how far afield you’re willing to acquire. In this regard, pursuing a local acquisition which can be consolidated into your facilities likely results the most synergies and the (relatively) easiest integration effort. Adding a second local office limits synergies and increases your fixed costs in uncertain times. It is also likely defocusing since you’re more than likely buying a business under financial stress which means extra attention will likely be required to make sure the acquired Solution Provider is put on a financially sound footing.

Finally, acquiring a prospect which is in another metro may present a significantly larger set of integration challenges, unless the business is highly additive with truly little chance of being further impacted by recession. These are the foundational rules to maximize the chances of success when considering adding a new location (i.e., a new geography):

- The “Distance Rule”: never open (or buy) a location farther away than this:

- You (the owner/CEO) can wake up in your home early in the morning, get to the location, have 3-4 meetings, and get back home in time for a late dinner.

- Any farther away than that, and you will not go often enough to make it successful.

- There needs to be someone in charge of the location. It should be your best general manager from your current location, who moves there.

- It should not be a new-hire manager.

- Assume it will take twice as long and cost twice as much, to bring the new location to acceptable growth and profit.

- Then re-decide whether it makes sense to do.

- Do not give yourself permission to open a new location until growth and profitability of your current location is at least at Median or better.

Performing the Search, Making an Offer, and Closing the Deal

Once you decide the profile of the Solution Provider that you’re looking for, you then need to decide how to target prospective Sellers and get them to engage with you. Think of the required effort as a marketing campaign, which is what it is. You’ll need to (a) build a database of the prospects in your target geography which, outside in, are most likely to meet your criteria; (b) build an outreach campaign to try to get these prospects to engage with you; and then (c) execute the campaign.

You can clearly perform these tasks yourself, if you have the necessary bandwidth and expertise on your team. Alternatively, you might approach a local business broker for a small deal (e.g., for a transaction where the price is less than $3-5 million) or a buy-side investment banker for larger deals, typically where the transaction price is at least $5 million.

Once you have a prospect engaged, how should you think about pricing and terms, now that we’re in a recession? We recommend you focus on a fair price, even in these recessionary conditions there could be multiple Buyers in larger metros and for Solution Providers of significant size. That said, you will likely find prospective Sellers where their cash flow (or EBITDA) has slid significantly and may perhaps even be negative. In this case, you’ll need to consider offering a price based on a multiple on Monthly Recurring Revenue (MRR) – prior to the current crises the most you might pay as a multiple of MRR would be in the range of 1.5 times.

Price aside, we can’t emphasize enough that in a recessionary environment, you need to focus on terms that provide absolute downside protection to you as a Buyer. The mechanism to provide such downside protections is an earnout, where portion of the price, or total consideration, is withheld pending earning out.

Seller’s Notes are an additional tool which can provide you with additional protection. With a Seller’s Note the Seller is effectively loaning you, the Buyer, a portion of the purchase price. This allows you to use less cash, allowing you to retain cash that you made need to weather the recession.

As you move to make an offer to a prospective Seller, make sure you set expectations with the Seller that you will be putting their business on a solid economic footing, most especially generating positive cash flow, at the outset and this will more than likely require staff reduction and potentially changes in compensation.

Finally, what to do if you don’t have the cash to buy? First you ought to revisit are you really in a secure enough position to be contemplating M&A? If you’re truly convinced you are, but need additional sources of capital to fund potential acquisitions there are a few options to consider:

- Consider offering stock in your business – aligns you and the selling owners, preserves some future upside for them and, most importantly, conserves cash which is a must do in a recession. Sellers may actually prioritize a safe harbor for them and their customers over cash with the ability to maintain a possible future upside;

- You may also be able to find local investors who are looking for investment opportunities during a recession – be forewarned though most of these capital sources will be looking for a bargain;

- We would not recommend taking on (additional) debt during a recession, though if your cash flow is secure enough that may be an option for you.

An Alternative Way to Do Smaller Acquisitions

The Buyer may want to consider doing smaller acquisitions, those say, under 6 or 8 people, as “group hires” instead of full acquisitions. The smaller Seller may prefer this approach as well. Acquisitions of this size can be done effectively. However, the full acquisition process – requiring a valuation, due diligence and an often-complex deal structure – can make deals this size impractical for the Buyer to do. As a result, a willing Seller may be passed up.

The gist of the “group hire” approach is that most, if not all, compensation to the Seller is low risk to the Buyer. This means the complexity of the deal can be minimized and still be safe for both parties. Here are the Buyer guidelines for a successful “group hire” transaction:

- Not “acquisition” but “group hire” of small competitors distressed or going out of business.

- The goal here is to reduce the Seller’s level of anxiety about the sale; make it easier and less emotional for both parties.

- To manage risk, <20% of Buyer’s size, not bigger.

- Buy the customer and prospects lists in exchange for a job for the former owner, enough cash to cover the Seller’s legal and accounting fees, and a 10% commission on accounts for one year.

- Seller also gets a good job with the Buyer’s company, and does their best to bring along desired employees.

- The Buyer should get pre-agreement that you can terminate your choice of customers; low OML Solution Providers often have a higher proportion of low OML customers.

- Remember, however, legally, this will still be an acquisition, with all the protections for Seller and Buyer:

- Non-compete from Seller, Reps and Warranties, etc.

- You still want to do a modicum of due diligence, etc.

Group hires are an affordable way to enable a successful transaction between a willing Buyer and a Seller looking for safe haven, a good job, and a fair payout for the Revenue generated by the assets they bring.

Insights for Sellers (and for Buyers)

If you’re really in trouble your best bet may be to simply speak to a handful of your local competitors and fold in your business and try to cut the best deal you can.

If you’re an owner that can go it alone but has decided there’s strength in size and financial resources, then best to run an actual process that’ll take several months. Even then be prepared for a deal with lower pricing, potentially substantially lower, that prevailed at the beginning of Q1 2020. Additionally, with a lower price, the prospective Buyers may still seek to protect their downside risk by asking the Seller to accept:

- An earnout

- Potentially a Seller’s Note

Your steps to identify a prospective Buyer are parallel to those outlined above for Buyers.

You’ll need to (a) build a database of the prospects in your target geography which, outside in, are most likely to meet your criteria; (b) build an outreach campaign to try to get these prospects to engage with you; and then (c) execute the campaign.

You’ll also need to prepare a memo that effectively markets your firm to prospective Buyers, and which does so in full recognition of the current conditions. Including:

- What’s the realistic “bottom” for your business on a Revenue, Gross Margin, and EBITDA basis?

- What is your customer base and how locked in are they, particularly in a recession?

- What solutions do you offer and why are these offers competitive and compelling?

- What are your core human capital strengths?

- What are the synergies a Buyer could expect in acquiring your business? Actually, try to calculate the benefits a Buyer might get from consolidation in G&A, facilities, and operations – note these synergies accrue to the Buyer not you as the Seller.

As with Buyers, you can clearly perform these tasks yourself, if you have the necessary bandwidth and expertise on your team. Alternatively, you might approach a local business broker if you’re likely going to sell for less than $3-5 million; or a sell-side investment banker if you have a realistic chance of selling your business for more than $3-5 million.

Summary

As a Buyer the current environment will undoubtedly present you with a number of opportunities to acquire Solution Providers. But caution is the order of the day; you may be catching a falling knife of some size, speed, weight and sharpness.

As a Seller, be prepared for a lower price on terms that protect them from a potential drop in your Revenue – e.g., for an MSP upwards of 25%. As such do your best to get multiple Buyers engaged as that will improve your chances of an acceptable outcome.